📋 Table of Contents

Jump to any section (15 sections available)

📹 Watch the Complete Video Tutorial

📺 Title: How AI Will Transform Accounting: A $100B Opportunity Explained

⏱️ Duration: 832

👤 Channel: a16z

🎯 Topic: Will Transform Accounting

💡 This comprehensive article is based on the tutorial above. Watch the video for visual demonstrations and detailed explanations.

Accounting is undergoing a seismic shift—one that most people aren’t talking about, despite its massive implications for businesses, professionals, and everyday taxpayers. While headlines focus on AI disrupting creative fields or manufacturing, a silent crisis is unfolding in the accounting profession: a dramatic shortage of talent, skyrocketing workloads, and outdated “Reagan Era” software that hasn’t kept pace with modern demands.

This comprehensive guide extracts every insight, statistic, trend, and prediction from an expert analysis of how artificial intelligence—particularly large language models (LLMs)—is poised to revolutionize accounting. From workforce demographics to software limitations, from AI capabilities to business model hurdles, we’ll explore why accounting is uniquely ripe for disruption and what this means for firms, professionals, and consumers alike.

The Looming Accounting Talent Crisis

One of the most critical yet underreported issues in professional services is the rapid decline in accounting professionals. According to industry data, 75% of Certified Public Accountants (CPAs) are set to retire within the next decade. Simultaneously, the rate of new CPA graduates is nowhere near sufficient to replace this exodus.

Compounding this problem, the total number of accountants in the U.S. has already dropped significantly: approximately 16% between 2019 and 2022. This isn’t just a minor fluctuation—it’s a structural collapse in workforce supply at a time when demand is surging.

Soaring Demand vs. Shrinking Workforce

While the number of accounting professionals is declining, the complexity and volume of accounting and tax work have only increased over time. Businesses and consumers alike require more sophisticated financial reporting, compliance, and advisory services than ever before.

This creates a perfect storm: firms face immense pressure to meet rising client demands with fewer staff. The result? Burnout, reduced service quality, and an unsustainable workload per employee. As one expert notes, “Your overall workload is remaining the same or increasing, but your number of staff that are hired and retained to perform that work is either remaining flat or declining.”

The Enormous Scale of the Accounting Market

Despite the talent shortage, accounting remains a massive economic sector. Consider these figures:

| Category | Workforce Size | Economic Impact |

|---|---|---|

| Accountants and Auditors | ~1.5 million | Part of a $100+ billion wage economy |

| Broader Accounting Roles (bookkeepers, payroll, corporate finance, etc.) | Over 3 million | Represents hundreds of billions in annual spending |

This vast market performs millions of hours of work annually—much of it repetitive and manual—creating a prime opportunity for automation and AI-driven efficiency gains.

Why Accounting Is Uniquely Ripe for AI Disruption

When evaluating professional services for AI disruption potential, experts look for three key traits:

- Highly paid professionals

- Performing repetitive tasks

- Tasks that could benefit from smarter automation

Accounting checks all three boxes “in spades.” Unlike creative fields where AI hallucinations can be creatively useful, accounting demands 100% accuracy—making it both a high-stakes and high-opportunity domain for reliable AI tools.

Accounting vs. Legal: A Tale of Two Professions

Legal services have seen rapid AI adoption, with tools like Harvey AI gaining widespread traction among top law firms. Accounting, despite similar underlying characteristics, has lagged behind.

One key difference: legal work is text-dominated, aligning perfectly with current LLM capabilities (text-in, text-out). Accounting, by contrast, is highly quantitative—centered on numbers, calculations, and structured financial logic. This may explain why AI adoption has been slower, though not impossible.

The “Why Now?” Moment for Accounting AI

Investors and innovators often ask: “Why is now the right time to invest in this category?” For accounting AI, the answer lies in converging demographic and technological trends:

- Mass retirements of experienced CPAs

- Insufficient new talent entering the field

- Mounting pressure on firms to maintain service quality

- Advancements in LLMs capable of handling unstructured financial data

These forces create urgent demand for software solutions that can fill labor gaps—not just with more humans, but with intelligent automation.

Real-World Industry Response: Firms Are Ready to Invest

The urgency is real. One top-20 accounting firm recently indicated it was prepared to spend up to $500 million—either building or acquiring software—to future-proof its operations. This signals a strategic shift: firms no longer view software as a cost center but as a core competitive necessity.

Moreover, professionals across the industry are in “resounding agreement” about the need for change. They want:

- Greater efficiency

- Happier, less overburdened staff

- A shift from “doer” to “reviewer” roles

AI’s Current Strengths in Accounting

While full automation of accounting is still emerging, LLMs already excel in specific, high-value tasks. Here’s where AI is making the biggest impact today:

1. Data Collection and Ingestion

Accountants routinely request clients to provide:

- General ledger exports

- Bank statements

- Receipts

- Vendor contracts (often as PDFs)

These documents exist in unstructured formats across disparate systems. LLMs are exceptionally good at parsing, interpreting, and normalizing this data—turning chaos into structured journal entries and reports.

2. Accounting Research and Guidance

When practitioners need to determine how to classify a transaction or interpret a GAAP (Generally Accepted Accounting Principles) rule, they traditionally rely on:

- Google searches

- Legacy research databases

Now, LLMs can provide robust, citation-backed opinions—referencing precedent cases, regulatory guidance, and alternative interpretations—far faster and more comprehensively.

3. Report Generation and Tax Filing (Emerging)

While still in early stages, AI is beginning to tackle automated financial report drafting and tax return preparation. Startups are now “rebuilding the tax engine using AI,” signaling a fundamental re-architecture of core tax software.

4. Client Advisory Services (Future Frontier)

The ultimate goal: AI that can synthesize financial insights and deliver proactive, strategic advice to clients. This remains in the “very early days,” but represents the highest-value application of accounting AI.

The Legacy Problem: Reagan-Era Accounting Software

Despite accounting’s ancient roots—tracking money has existed since the dawn of commerce—the software supporting it is shockingly outdated. Experts describe current tools as “Reagan Era software,” developed decades ago with minimal innovation.

Even consumer tax products—many of which still existed as CD-ROMs just 10 years ago—have seen only marginal improvements. Both professionals and end-users suffer from clunky, inefficient systems that fail to leverage modern computing power.

Hurdles to AI Adoption in Accounting

Despite enthusiasm, several significant barriers slow AI integration:

1. Zero Tolerance for Errors

Unlike creative fields where AI “hallucinations” can spark ideas, accounting demands absolute precision. A single error in a tax return or audit can have legal and financial consequences. Firms are therefore extremely conservative about deploying AI tools in production environments.

2. Billable Hours Business Model Conflict

Most accounting firms operate on a billable hours model. If AI allows a task to be completed in 20% of the original time, logic dictates that billing should drop proportionally. But this creates a short-term revenue threat.

However, experts believe market forces will push the industry toward fixed-fee engagements. Firms that leverage AI to deliver high-quality work at lower costs will gain competitive advantage—forcing the entire sector to evolve.

3. Buyer Misalignment

Selling AI to accounting firms requires targeting the right stakeholder:

- Individual contributors may fear obsolescence: “You’re trying to make me obsolete.”

- Firm leadership sees clear ROI: reduced labor costs, higher capacity, improved margins.

Successful AI vendors must position their tools as force multipliers—freeing professionals from drudgery so they can focus on high-value advisory work.

The New Software Distribution Model

Historically, accounting software companies succeeded by selling through accountants to end-clients. Examples include:

- Bill.com

- Sage

- Intacct

These tools were adopted because they made the accountant’s job easier, and accountants then “prescribed” them to clients.

A Paradigm Shift: Selling Directly to Firms

Today, for the first time, software companies can build massive businesses by selling directly to accounting firms themselves. Why? Because LLMs can now interpret complex accounting rules and logic without requiring armies of CPAs to manually encode them into software.

In the past, venture-backed accounting software startups needed “80 accountants in a room” to translate regulations into code—a costly, slow process. Now, engineers paired with LLMs can automate much of this, drastically lowering development barriers.

What This Means for Consumers and Businesses

The ripple effects of accounting AI will benefit everyone:

- Lower prices: Reduced manual labor should translate into more affordable services.

- Faster service: Automation accelerates data processing and report generation.

- Better experiences: Professionals spend less time on data entry and more on strategic advice.

Remember: under the billable hours model, clients already pay for every minute of manual work—even if it’s invisible. AI removes this hidden cost, delivering more value at lower prices.

The Future of the Accounting Profession

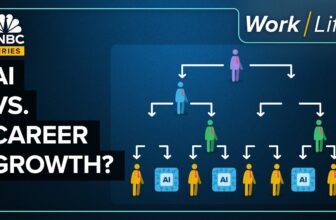

AI won’t eliminate accountants—it will transform their roles. The future belongs to professionals who evolve from “doers” (data entry, classification) to “reviewers” and “advisors” (interpretation, strategy, client relationships).

This shift aligns with natural career progression and addresses the core reason many enter the field: to provide meaningful financial guidance, not to wrestle with spreadsheets.

Key Takeaways and Action Steps

- 75% of CPAs will retire in the next 10 years; new graduates aren’t replacing them.

- Accounting work is growing in volume and complexity, straining firms.

- The U.S. accounting ecosystem employs over 3 million people and represents $100B+ in wages.

- Current accounting software is outdated—many tools haven’t meaningfully evolved in decades.

- LLMs excel at data ingestion and research but require 100% accuracy for financial outputs.

- Billable hours models create short-term friction but will give way to fixed-fee pricing.

- Firms are ready to invest heavily—up to $500M—in AI solutions.

- Consumers will benefit from lower costs, faster service, and better advice.

Final Thoughts: Embracing the Inevitable

As Benjamin Franklin famously said, “In this world nothing can be said to be certain, except death and taxes.” Accounting touches every individual and business—making its transformation one of the most impactful yet overlooked AI revolutions.

The convergence of demographic collapse, technological readiness, and market demand means AI will transform accounting—not in the distant future, but right now. Firms that embrace this shift will thrive; those that resist risk obsolescence.

For professionals: view AI not as a threat, but as a tool to reclaim your time and elevate your value. For consumers: expect better, faster, and more affordable financial services. And for innovators: the opportunity has never been greater to rebuild one of the world’s oldest professions with the power of modern intelligence.